Orchard Funding Group

A safe, nano-cap lending institution trading at 3.5 times earnings and 1/3rd of book value with a possible near term catalyst

Disclaimer: None of what I write is a recommendation to buy or sell a stock. I am an internet stranger writing about random businesses with no successful track record in investing. This is a selfish endeavor to grow as an investor myself and to document my research as I do not have a good memory. Please do your own research before buying a stock.

Update(5/16/24): I exited my position in Orchard and have explained here in more detail.

If you like reading pdfs, here is a pdf version of this writeup.

Thesis - The Shorter Version

Orchard Funding Group, a lending institution, whose core loan product(insurance premium financing) is an essential product with extremely low credit risk, very low interest rate risk(close to 80% of loans in the loan book are less than a year in duration), which has a conservative adjusted debt to equity ratio of 1.7:1, a 20+ year history of operating successfully, with a demonstrated history of consistent profitability in the past 10 years(at least) and an average Non Performing Assets(NPA) ratio of 0.3% in the past 10 years, trades at 3.5 times 2023 earnings, one-third of book value and a 10% dividend yield.

This idea is really as simple as that. If you want to learn more about the company and unpack the previous paragraph, keep reading but I believe this is all there is to this investment thesis.

Warning: This company is a highly illiquid nano-cap, so any trades should be placed as limit orders.

Business Description

Orchard Funding Group is a provider of insurance premium finance, professional fee finance and a few other lending products, in the UK. The company has been in operation since 2002. Insurance premium finance allows consumers and businesses to spread out the cost of insurance premiums(like home insurance premiums) over 6-12 months(typically), instead of having to shell out an annual premium all in one go. This is the core product of Orchard.

Orchard lends to clients via insurance brokers, who sell insurance products to their clients. The consumer gets to spread out their annual premium payments, the insurance broker(insurer) gets the annual premium immediately and Orchard, as a lender, earns interest on the loan. Professional fee finance, similar to insurance premium finance, allows clients of accounting firms, law firms etc to spread their fee payments to these firms.

Insurance Premium Finance

There are 4 parties involved in an insurance transaction - the client, insurer, insurance broker, and the insurance premium finance credit provider(Orchard). There are two forms of insurance premium finance lending by Orchard, indirect and direct. In the indirect way, Orchard funds the brokers and they in turn lend money to their clients using their own lending company called “Premium Finance Company(PFC)”. In this case, Orchard forms the lending’s backend(premium finance credit provider) whereas the front-end(what the customer sees) is the PFC, which is an entity owned by the insurance broker. These terminologies can be confusing but it does not matter for the thesis. In the direct way, Orchard acts as the direct lender to the clients. See the diagrams below for more clarity.

I believe there is not much of a difference between the two forms of lending practically, apart from the fact that the indirect form adds broker commissions and fees which the direct form lowers.

Insurance Premium Finance is one of the safest lending products one could imagine. The primary risk one should be worried about in a lending product is credit risk. This is kept to a minimum for insurance premium financing and almost non-existent in many cases. The lending is structured in a great way(I believe the following is the structure for both the indirect and direct forms). The brokers act as a guarantor for its clients, so if a client defaults, the insurance broker is liable to pay. If a broker suddenly became bankrupt, the clients are still liable to pay Orchard(even in the indirect form). Moreover, Orchard mostly does premium financing for refundable/cancellable policies. So if a client stops paying, the policy is canceled and the insurance company refunds the premium payments prorated for the policy’s remaining duration.

Let’s say the insurer goes out of business. In the UK, the Financial Services Compensation Scheme(FCCS) protects individuals from failure of financial institutions(similar to FDIC/SIPC in the US). As per this scheme, the UK government will pay the client 90% of the insurance premium he/she had paid to the failed insurance company for an insurance policy. Now, if the client had taken financing for paying his/her insurance premiums, the government is liable to pay 90% of the insurance premium to the premium finance company - which is Orchard in our case. One can easily see why this type of lending product is one of the safest. The 2015 annual report(first as a listed company) indicates that the company did not have any bad loans from 2008-2015(which included the financial crisis) and has had impairments of only 0.3% of the loan book in the past decade.Also, 80% of Orchard’s loans are less than a year in duration, thus avoiding interest rate risk.

Orchard’s current funding sources are mainly Toyota Financial and to a smaller extent - Natwest Bank and bonds. To minimize liquidity risk, Orchard maintains a very conservative debt to equity ratio of 1.7:1(after adjusting for approx $12M of loans on its balance sheet from Toyota Financial which has zero credit risk - yes, it is zero), with room to expand its lending in the future. Orchard’s funding sources would indicate that its cost of funds are on the higher side and are not as low as a bank.

One more thing to keep in mind is Orchard’s insurance premium finance is mostly an essential type of lending(to essential insurance policies like home insurance etc), and customers often need these products more in times of crises. This makes the company resilient in times of recessions - the company was still very profitable during covid and one of the CEO’s letters to shareholders mentions that the company was resilient during the 2008 financial crisis as well.

Management

Ravi Takher, the founder and CEO, owns 54% of common shares outstanding. Orchard has paid consistent dividends amounting to at least 1/3rd of earnings every year, has retained the remaining to grow the loan book conservatively at a decent RoE(around 10%) and kept NPAs very low with great underwriting discipline(0.3% of loan book on average in the past decade). Orchard has not burnt shareholder capital on any expensive acquisitions in the past and have made investments like software in-house and at minimum costs. Orchard has expanded into other segments like school/leisure financing very slowly(fast expansion for a lending firm into new segments can often bring trouble) and many of these new segments possess a lot of the low-risk aspects of its core premium financing business.

In addition, Ravi Takher has done a great job for a nano-cap company in the quality of its disclosures in its annual reports and explaining Orchard’s business economics and competitive dynamics through his shareholder letters. Orchard has not raised any new capital ever since its original listing in 2015 and there has been no shareholder dilution. I recently came across an old Paul Andreola article on shareholder structure - and the points in that article seem very applicable to Orchard, considering its low outstanding share count(as mentioned in the next section). For all of these reasons, I believe this is a quality management team(and CEO), especially considering Orchard’s size(market cap of £6M).

Valuation

Orchard has about 21.3M shares outstanding and trades at a market cap of £6.1M(or 29 pence per share). The company’s book value(equity) is £17.8M - in other words, it trades at close to 1/3rd of equity value. The company earned 8 pence per share in 2023 and trades at 3.5 times trailing earnings. Orchard has paid 3 pence per share of dividends annually in the last few years. So, the company trades at a 10% dividend yield.

The company is in the lending business, so it does employ leverage. However, the adjusted debt to equity ratio is still a comfortable 1.7:1 currently. The company can suffer a haircut in its adjusted loan book of 25% and still be worth its current market price. One can see that with leverage, even if a company trades at 1/3rd of equity value, it still does not mean its enterprise value can drop by 2/3rd and still be a profitable investment. That is why the ultra low risk nature of its insurance premium finance operation is core to this thesis. So if this opportunity is so good, why has the market priced it at 3.5 times PE and 1/3rd of book value?

Possible Concerns

Firstly, in February, the FCA(Federal Conduct Authority), a regulatory body for financial markets in the UK, has imposed a temporary ban on insurers selling new GAP(Guaranteed Asset protection) insurance policies for cars in the UK sold through dealerships. In the case a consumer has his car totaled, GAP insurance policies help cover the difference between what they owe on their car and the car’s current value. This is a useful product but the FCA doesn’t like the fact that insurers only pay out around 6% of premiums in claims whereas in the most extreme case, around 70% in commissions to auto dealers(who sell these products to the consumers). GAP insurance policies have a term of 3 years and form 20% of the loan book for Orchard currently. Note that these policies still have a lot of the favorable characteristics mentioned earlier about premium finance and hence are not liable to any credit risk. The ban means that Orchard will have to reposition their GAP part of their loan book into other insurance products, as the repayments come in over the next 3 years. They have grown year on year in revenues and loan book, so I believe they will have opportunities to do this. Nevertheless, this doesn’t justify a deep discount to their book value, considering they are not facing any losses on these loans(which are already very safe as mentioned earlier). Moreover, this likely is a temporary ban as the FCA wants to see the commissions to dealers go down, rather than permanently banning a useful product.

Secondly, in March, Orchard found a fraudulent loan on their books, which they mentioned was worth 500k pounds. In the latest half year update, this amount was adjusted down to 390k pounds and was mentioned that their loan book was verified to not have any more such instances currently. In a lending institution, bad loans do happen from time to time. This is not the first time it has occurred at Orchard - another instance happened in 2018(mentioned in Orchard’s 2018 annual report). Despite all this, Orchard has maintained an average NPA of 0.3% over the past decade. This tells me the underwriting has been pretty solid over the years and the latest event is likely one-off. These are the 2 major events that happened recently and the market seems to have overreacted to both.

Apart from this, DeepValueStonks on twitter, has done a great job writing up the company and also talking with some exiting shareholders on the other side of the trade. According to him, one of the reasons existing shareholders sold off were that they were disappointed with Ravi Takher’s lack of communication with the market. Ravi Takher, in his shareholder letters and through a number of well written older blog articles on BexHill’s site, offers a great view of the business economics.

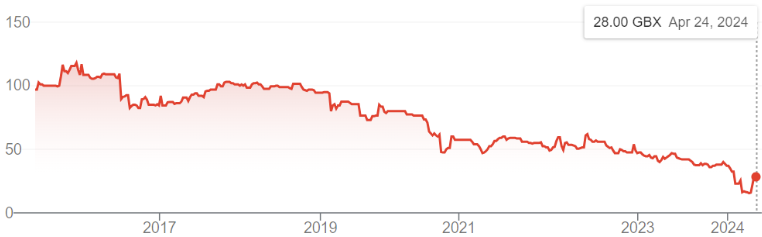

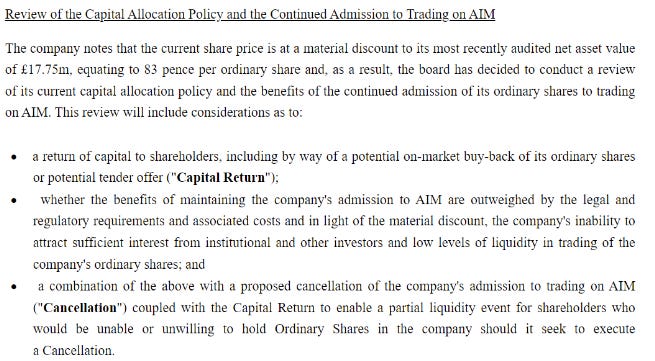

If you look at the chart of Orchard’s share price above, the share price has steadily dropped, from trading at a premium to book value at the time of listing to 1/3rd of book value currently and separating from fundamentals. The exiting shareholders are likely disappointed that not enough has been done by the management to make the market realize the true value of their holdings. Another reason that the shareholders have exited is that in the latest half year results update, the management has indicated that the company is contemplating delisting its shares from the exchange as shares have been trading at a significant discount to its book value of 83 pence per share. Below is this section of the press release.

It was also mentioned that the CEO, Ravi Takher, has informed the board that he may look to acquire shares in the open market. Ravi currently owns 54% of the shares outstanding and maybe he is looking to acquire enough shares to consider a delisting(75% of votes are needed for a delisting). So the current shareholders were scared that they may end up holding illiquid shares in case Ravi takes the company private without giving a chance for minority shareholders to make an exit. From reading the update above, it seems as though they are considering an exit option for shareholders who do not want to hold shares in the company after it is delisted.

The current management, in their recent press release, clearly point out that the shares have been selling at a big discount to book value. Also, Ravi Takher, likely does not want to spoil his reputation and future access to capital markets(he has been in the finance industry all these years and he is still only 60 years old) by ripping off minority shareholders. Nevertheless, I feel very comfortable holding Orchard, whose loan book consists of extremely low risk loans, at 1/3rd of book(equity) value. I believe that shares will likely not be taken private at a price below this.

What happens if minority shareholders are not given an option to exit? Well, considering the underwriting history of Orchard, and the attractiveness of their loans, I would be comfortable holding a company that has been steadily growing in a large market without taking on unusual amounts of risk or burning money on acquisitions, with a consistent track record of profitability and safe underwriting, which I purchased at close to a 30% earnings yield, 10% dividend yield and at 1/3rd of book value.

Premium Finance Scrutiny by the FCA

The businesses in the insurance premium finance industry in the UK are regulated closely by the FCA. Firstly, this scrutiny is not new. I found the following in Orchard’s 2015 Annual Report:

“The FCA recently reviewed the premium finance market and has revealed that insurer and insurance intermediaries have not always provided customers with clear information about different payment options available when buying general insurance products, including providing clear information about the overall cost of paying for insurance, clear information about the payment options available to them and transparency in the role of the intermediary. The board is confident that our documentation and procedures fulfil the requirements of the FCA, as evidenced by Bexhill UK Limited obtaining full FCA permission”

Of late, the FCA has been increasing scrutiny on this industry due to high interest rates charged by some premium finance providers to consumers. This is because many insurers pay commissions linked to interest rates for these premium finance products. This incentivises the insurance brokers to charge high interest rates for consumers in order to earn high commissions. Orchard’s CEO, Ravi Takher, has been vocal about this issue through his blog articles on BexHill’s website and his comments in industry publications. Orchard deals with smaller broker intermediaries as compared to the bigger players in this industry who deal with larger brokers and I believe Orchard does not engage in an interest-linked commission structure as the CEO has been standing publicly against these brokers that do. Moreover, in the 2023 Annual report, Orchard has indicated that it has had no instances from the FCA of non-compliance with regulations.

Based on a recent interview with Matt Brewis(Director general of insurance, FCA) in an industry publication, the FCA realizes that this is an essential product that cannot be banned(think people paying for car insurance, home insurance etc where consumers are already stretched financially due to the current inflationary environment and higher interest rates). The likely plan of action is to probably make an example of a few large firms that indulge in bad practices.

I believe that this might even work to the advantage of smaller players like Orchard, which has been playing on an unequal playing field against larger industry competitors(insurers/larger premium finance competitors) who indulge in practices like paying advance commissions to brokers to sell their products exclusively(a practice that Orchard does not indulge in and Ravi Takher has been openly critical about). Over the past few years, the FCA has been tweaking rules for the industry to ensure brokers sell policies that provide value to customers and ones that customers can afford. I also think Orchard has been quite proactive in terms of good practices that the FCA would like. For example, Orchard has been investing in developing Open banking, a software platform for insurance brokers to analyze the ability of a customer to afford a given policy before making a loan.

Even if one assumes all hell will break loose suddenly and the FCA totally bans insurance premium finance(looks highly unlikely), I believe the Orchard management with a demonstrated capital allocation discipline, will take the right steps to realize at least more than 1/3rd of book value to shareholders, for a company selling a very low risk loan product. In simple terms, 1/3rd of equity value seems like a very big discount to liquidation value, even if one assumes Orchard is faced with big fines from the FCA(again looks very unlikely).

Pre-mortem

I usually try to think of scenarios in which I could lose money before making an investment. These are some of the ways this thesis could go wrong.

FCA finds some questionable practices in Orchard’s lending business and levies fines which are big enough to affect book value in a significant way, although I believe this is not likely

Orchard may loosen underwriting standards for the 20% of total assets that it may have to redeploy from GAP insurance into other product lines

Orchard plans to expand in newer products like longer term asset lending and bridge loans which are longer duration. One good thing though is that these are secured against assets/properties unlike insurance premium financing which are “unsecured”(even though they are “unsecured”, I consider them to be safer) - this risk comes into play in case the delisting does not happen and I own the company for longer.

As I have mentioned earlier, Ravi Takher might take the company private without offering an exit to minority shareholders or by buying them out at a discount to current market value.

Final Thoughts

Overall, I believe the market has overreacted to some of the recent events. Considering the nature of insurance premium finance and Orchard’s track record of capital allocation, the company should be worth at least book value(equity) in almost all circumstances(definitely greater than 1/3rd of book value). I believe there is sufficient margin of safety in the current market price and the fact that there may be an imminent catalyst in the form of a delisting, makes it even more attractive as a special situation play(the board has also paused its dividend to review a delisting possibility). Even if the delisting doesn’t happen, I feel it is still a very good buy at current prices to hold for the longer term with no imminent catalyst(value being its own catalyst long term).

Disclosure: Long ORCH.L